When we look up the net worth of famous billionaires like Oprah Winfrey and Elon Musk, the figures we see do not look anything like ours can be compared with. But then, have you tried comparing yours to your peers?

*As an Amazon Associate I earn from qualifying purchases. This post may contain affiliate links from Amazon or other publishers I trust (at no extra cost to you). See disclosure for details.

There is a wide range of factors responsible for individual net worth. And these factors include location, age, race, investment assets, level of education, and bank account balances.

What Is Net Worth?

Net worth is the value of assets you have after everything you owe has been deducted. This metric is very vital to individuals and organisations to help gauge their strength using important data from their present financial position.

In business, net worth is otherwise referred to as shareholders’ equity or book value. There is a category of people who are referred to as high-net-worth individuals (HNWI), and they are people who have substantial net worth.

What Is Average Net Worth

Average net worth is the figured net worth of a group calculated into one. The median net worth is the middle value of all the given figures.

The average net worth helps to have a handy picture of how wealth is being shaped across a geographical location. The Federal Reserve Board reveals information about net worth, family incomes, and much more through a Survey of Consumer Finances released every three years.

The most recent data was issued in September 2020, and it reveals data collected in 2019. The data covers the overall average net worth of U.S. households put at $748,800.

Well, that figure is actually high because affluent households influenced it.

The median value is a bit more accurate to the net worth of the regular American citizen. The U.S. family has a median net worth put at $121,700.

How Is Net Worth Calculated?

Net worth is calculated by deducting all your liabilities from your assets.

A liability is a financial obligation or debt that diminishes the resources of an individual or a corporation. Examples include mortgages, loans, credit card balances, home equity lines of credit, installment loans (including student loans and auto loans), and accounts payable (AP).

Assets are everything you own that has monetary value. They include the value of your stock portfolios, money in your bank accounts, and also the current market value of properties you own such as cars, jewelry, houses, and art.

There are some categories of assets included by the Federal Reserve and they are:

- Retirement accounts. And it includes IRAs, 401(k)s, and 403(b)s.

- Real estate, including place of residence.

- Annuities with equity and cash value life insurance policies.

- Savings bonds, CDs, and government bonds.

- Bank accounts – savings, checking, brokerage cash accounts, money market accounts, call accounts, and prepaid debit cards.

- Health savings accounts

- Motorcycles, RVs, boats, vehicles including cars, and helicopters.

- Investment accounts which include individual taxable investment accounts and 529 college savings plans.

When your net worth is described as positive, your assets exceed your liabilities. And when they are described as negative, your liabilities exceed your assets. An individual or company has good financial health when they have increasing net worth.

On the other hand, decreasing net worth indicates bad financial health, and calls for quick attention.

Is Calculating Net Worth Necessary?

While net worth may not be an accurate figure of the subject, it is however a good way to figure out the weaknesses and strengths of a person or a company. And it doesn’t mean that because someone has a high net worth means that they have a high standard of living.

For instance, the home a person has may boost their net worth, while they may still be poor in cash.

Now, when we become curious about the net worth of others, we are very likely to get motivated to increase our speed in pursuing financial goals. But then, this is capable of making us feel unnecessarily inferior too.

Always take note that net worth is not a fixed figure. It can change positively or negatively with time.

How To Improve Your Net Worth

To improve your net worth, the best approach is to cut down your liabilities and improve or retain the level of your assets.

But then, bear in mind that we all have different net worth goals, and these goals ultimately depend on your financial targets. So, while you review your average net worth by age, keep in mind your basic objectives.

Proven Tips To Increase Your Average Net Worth

a. Settle all debts: Your debts can be used in increasing your net worth. Settle all debts as quickly as you can, but ensure to put into consideration penalties that could be connected to paying debts – such as mortgage – early.

b. Put your cash savings in places it will generate interests: Consider putting your savings into accounts that will produce interests for you. Or better still, invest the cash.

c. Make smart investments: Making smart investments doesn’t have to be in stocks alone. But purchasing a house or car that is within your financial capacity and is capable of giving you a long-term benefit should be considered, while also keeping all luxury expenses low.

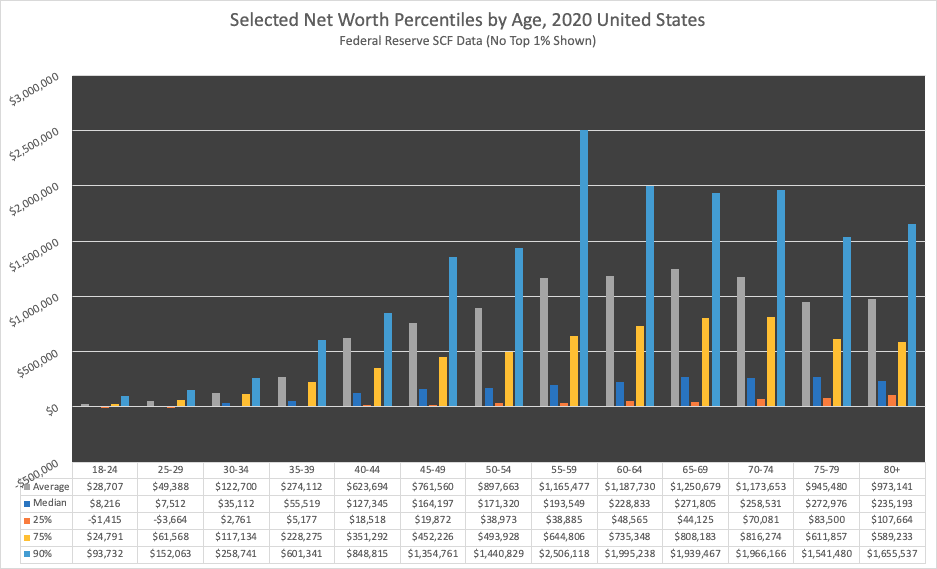

Recent data revealed by the Federal Reserve’s 2019 SCF which consists of a 14-month survey – February 2019 to April 2020 – published in September 2020 details average net worth by age.

| Age | 18-24 | 25-29 | 30-34 | 35-39 | 40-44 | 45-49 | 50-54 | 55-59 | 60-64 | 65-69 | 70-74 | 75-79 | 80+ |

| Median Net Worth by Age | $8,216 | $7,512 | $35,112 | $55,519 | $127,345 | $164,197 | $171,320 | $193,549 | $228,833 | $271,805 | $258,531 | $272,976 | $235,193 |

| AverageNet Worth by Age | $28,707 | $49,388 | $122,700 | $274,112 | $623,694 | $761,560 | $897,663 | $1,165,477 | $1,187,730 | $1,250,679 | $1,173,653 | $945,480 | $973,141 |

| 90% | $93,732 | $152,063 | $258,741 | $601,341 | $848,815 | $1,354,761 | $1,440,829 | $2,506,118 | $1,995,238 | $1,939,467 | $1,966,166 | $1,541,480 | $1,541,480 |

| 75% | $24,791 | $61,568 | $117,134 | $228,275 | $351,292 | $452,226 | $493,928 | $644,806 | $735,348 | $808,183 | $816,274 | $611,857 | $589,233 |

| 25% | -$1,415 | -$3,664 | $2,761 | $5,177 | $18,518 | $19,872 | $38,973 | $38,885 | $48,565 | $44,125 | $70,081 | $83,500 | $107,664 |

How to Determine Your Average Net Worth By Age

Take control of your financial situation by understanding what your net worth should be as regards your age.

For you to achieve that, you should make a comparison of the average net worth of your American peers. Then give yourself a target of where you aim at being in say, 5years, 10 years, 20 years, or at retirement. Then do your calculations to ensure you are on the right path towards your goal.

What Should Not Be Classified Towards Net Worth

a. Equity in your primary residence

Technically, we can say that equity in your home counts towards your net worth. But then, it doesn’t count towards investable net worth.

That kind of cash cannot be used in building wealth or making investments. If you sell your house, a part of that equity stays as cash. The only way to take out cash for investing is to take on debt, which also offsets the money and some.

b. Liabilities

When you have things that cut down your net worth, they cannot be counted towards net worth.

After calculating your investment assets, deduct your debts, loans, and every other liability there is – including student loans, credit card balances, personal loans, business loans, and others.

More so, if you owe beyond the worth of your assets, then put together the negative equity as liability.

c. Personal cars

Your cars cost you cash to maintain. They are part of the expenses you incur in transportation. Their value drops, and the more you keep throwing cash at them the less likely it is that they would yield commensurate worth when valued.

d. Personal belongings

Having all the expensive jewelry, wristwatches, and other personal stuff may make you feel very rich, but then, selling out those stuff will give you a clearer picture of the value those personal items actually hold.

Tips To Move Up To The Upper Middle Class

a. Max out your IRA and/or 401k as soon as you can. Make a savings of an equal or greater amount reflected in after-tax investments as well.

b. Relocate to an area in the country where there are bigger opportunities. Consider areas that can help give you a boost in your financial situation with business opportunities and robust employment.

c. Seek financial help when necessary. You could also consider hiring a professional to give you financial advice in managing your income and expenses.

d. Invest, invest, invest. While you are working, ensure to make as many investments as you can.

e. Look into the proper asset allocation in connection to personal risk. Your assets should be placed in such a way that focuses on beating the risk-free rate of return by up to two to three times.

f. Gain a lot of knowledge about investing, taxes, wealth management, retirement, and other financial metrics.

g. Purchase a home that is affordable and would remain yours for a very long time.

h. Insure your house, health, vehicles, life. Many times we can’t control situations that can easily wipe off our net worth.

g. Employ necessary tools to track your finances. Ensure to adequately measure your finances and block off any kind of leakage that may be.

h. Think and believe in the possibility that you can become wealthier and deserve the wealthy life.

Featured on: Fit Small Business, Romper,UpJourney, Link2Us Mag, and lots more!

- 19 Best Work From Home Part Time Jobs for College Students - October 24, 2024

- 18 Legit Apps To Earn Gift Cards (& real cash!) - October 24, 2024

- 15+ Amazing Game Apps That Pay Instantly To PayPal - October 23, 2024